Your worldwide refrigerant partner

Get in touch with usBeyond the Ban: Proactive Product Portfolio Adaptation Under the F-Gas Regulation's New Prohibitions

The European Union's F-Gas Regulation (EU) 2024/573, which became applicable on March 11, 2024, signals a definitive and urgent shift towards eliminating potent fluorinated greenhouse gases (F-gases) from the EU market. This ambitious target of zero permissible HFCs by 2050 is not solely reliant on quota reductions; it is critically supported by a series of new product prohibitions designed to compel the market's transition to low-GWP or natural refrigerant alternatives. For importers, these phased bans are a game-changer, demanding immediate and proactive adaptation of their product portfolios to avoid severe financial losses and maintain market access.

The regulatory intensification is rooted in the alarming climate impact of F-gases, whose emissions doubled between 1990 and 2014, contrasting sharply with reductions in other greenhouse gases. The Intergovernmental Panel on Climate Change (IPCC) has emphasized the critical need for global F-gas emission reductions of up to 90% by 2050 to keep global warming within the 1.5°C target. The EU's response, Regulation (EU) 2024/573, directly addresses this imperative by closing existing loopholes and accelerating the transition to climate-friendly alternatives.

The Expanding Scope and New Prohibitions

The new regulation significantly expands its scope, now encompassing a broader range of products and equipment that contain F-gases or whose functioning relies upon them. A notable inclusion is metered dose inhalers (MDIs), previously exempt, which are now explicitly integrated into the HFC quota system, thereby broadening the regulatory net to a critical healthcare sector.

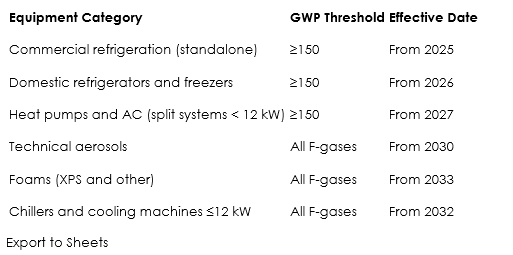

Crucially, the regulation introduces new prohibitions on placing certain equipment on the EU market, with bans on various products based on their GWP levels coming into effect gradually between 2025 and 2035. These bans are strategically designed to force the market's transition to low-GWP or natural refrigerant alternatives.

Key prohibitions include:

Strategic Imperatives for Importers

These phased bans compel manufacturers and, consequently, importers to proactively reassess and redesign their product portfolios, driving significant investment in alternative technologies. Failure to do so risks leaving non-compliant inventory unsellable and incurring substantial financial losses.

To successfully navigate these impending prohibitions, importers must adopt a proactive and comprehensive adaptation strategy:

- Immediate Product Portfolio Assessment: Importers must immediately assess their current product offerings against the new prohibitions, paying particular attention to the ban on high-GWP commercial standalone refrigeration taking effect from 2025. This involves understanding the GWP of refrigerants in all imported equipment.

- Collaboration with Manufacturers/Suppliers: Work closely with manufacturers and suppliers to understand their transition plans and to ensure that future product lines will comply with the new GWP thresholds and bans. This may require influencing product development and supply chain adjustments.

- Investment in Alternative Technologies: Importers should strategically invest in or source equipment that utilizes compliant, low-GWP alternatives or natural refrigerants. This is not just about compliance but about securing a competitive edge in a market increasingly favoring sustainable solutions.

- Inventory Management: Implement robust inventory management strategies to minimize the risk of holding unsellable, non-compliant stock once bans come into effect. This includes careful forecasting and potentially accelerating the sell-off of high-GWP equipment before deadlines.

- Market and Demand Forecasting: Anticipate shifts in market demand as the availability of high-GWP products diminishes and consumer and industry preferences move towards more sustainable options. This foresight positions businesses as leaders in environmental responsibility, enhancing their market reputation and opening new business opportunities in a rapidly evolving, greener economy.

By proactively adapting their product portfolios to align with the F-Gas Regulation's new prohibitions, importers can transform what appears to be a regulatory burden into a strategic advantage, ensuring continued market access and long-term business success in the EU.